Victoria Police Capability Development Building Project

Author: manager

Victoria Police Capability Development Building Project was successfully completed and officially opened by the Police Minister on 26th April. This building has been designed to facilitate the domestic violence training centre as well as office space.

Mitchell Brandtman is assisting John Holland to deliver a state of the art project in the smartest possible way.

Stage 1 of Macquarie Square, a new commercial precinct on Waterloo Road in Sydney is, and will be a full digitally engineered project from Design Development through to Operation. BIM (Building Information Modeling) at its best!

Our 5D Cost Planning team have been leveraging the 3D design models by applying our unique 5D (cost) and 4D (time) data workflows to provide linked cost plans, visual trade packages and scope change assessments and are currently delivering the progress assessments by utilising our 5D+4D data and 3D laser point-cloud scanning to precisely quantify and value the physical work complete on site and track progress. Virtual cash flows are also being run to provide milestone insight into cost and project progress with the team at Solid Support.

Mitchell Brandtman is proud to be working on this key project for John Holland, targeted for a 5 Star Green Star rating and an energy performance target of 5 Star NABERS rating.

With the overwhelming success of our Developer workshops in 2018, Mitchell Brandtman has decided to once again host a number of Education workshops for Developers.

Sometimes the role of the Financiers QS is not fully understood and often there can be uncertainty around the requests for information and documentation the QS needs to provide the Financier to secure funding . In running the workshops, our aim is to share our knowledge on this with the outcome being that the process that needs to happen between the Developer and their Financiers QS will be streamlined.

DA

BA

Contracts (GMP, Cost Plus, D&C etc) and Insurances

Drawings

Budgets/Contingency etc

Estimating/ cost $m²

Other topics covered will include:

Elemental benchmarking

Different Types of variations – base building, developer initiated, purchaser variations

Assessments v Certificates

Bank Guarantees/Ins Bonds/Cash

BCIPA

Click on the workshop dates below to register

15th May FULL 12th June FULL 17th July FULL

Please note that these sessions book out quickly!

If you have any questions in regard to the Developers Education Program please email Sophie Clarke at sclarke@mitbrand.comor call direct at 07 3327 5001.

We look forward to sharing our knowledge with you and your team.

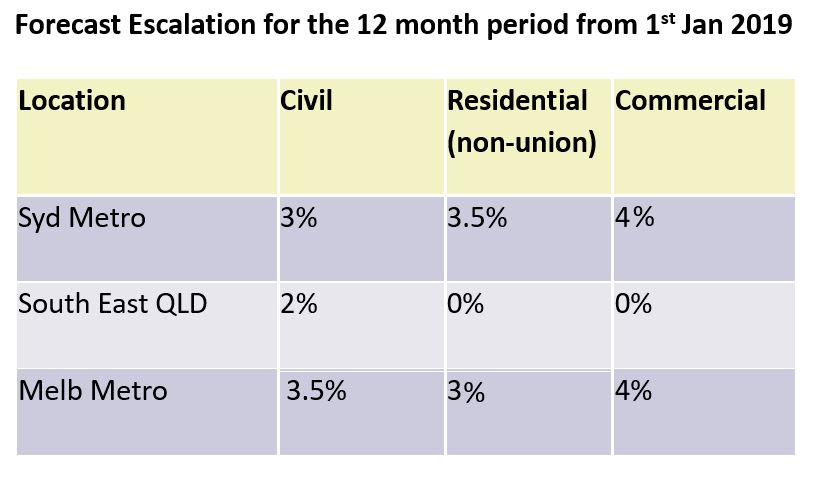

Despite increasing political headwinds, and market uncertainty, Developers who develop for a living still need to be able to make their projects stack up. Mitchell Brandtman explores how construction costs will likely impact different sectors across the East Coast of Australia and gives their escalation forecast for 2019.

National Commentary

State and Federal elections are looming and bringing with them both promises and fear-mongering which in equal parts discourage Developers and purchasers alike, and put downward pressure on property values and confidence. This is on top of markets moving from record activity into decline, slowing GDP, low wage rises, and a per capita recession.

Despite the challenges being faced in the private sector markets over the next few years, we will continue to see the major East Coast cities evolve with significant public spend underway on major committed infrastructure projects. Commentary often focusses on the market impacts of this Public spend on major projects. There is no doubt that infrastructure and landmark precinct buildings can have an impact on costs – in particular in already heated markets, and for materials that are in high demand by different sectors. However through monitoring key activity data we know that fluctuations in broader construction costs are more closely correlated to demand in residential construction.

If labour is a key component then contractor and sub-contractor confidence is a leading indicator of what is going to happen. Right now in almost every major centre, residential contractors are worried that their current workload is greater than their future workload. Will this lead to an immediate drop in the construction cost per dwelling? No – however it will change the balance of power away from sub-contractors back to head contractors, and will give Developers something that they have found lacking in the previous cycle – greater competition. We know that markets take time to adjust and to find their new normal, so we expect to see widened tender price spreads across most sectors and a continued difference between expectation and on the ground experiences when it comes to current and future costs. Though one thing is for certain, the upcoming markets won’t allow for any ‘fat’ that may have crept in through the boom times. It’s time to get sharp again.

Market commentary is that the Sydney and Melbourne markets are into the downturn cycle and that Brisbane has bottomed out. If this is the case then what we are still likely to see are all three of these markets ending this cycle at a level higher than their long term average approval rates. The point to note here is that post decline there will still likely be a similar amount of work under construction as was near the top of the previous cycle.

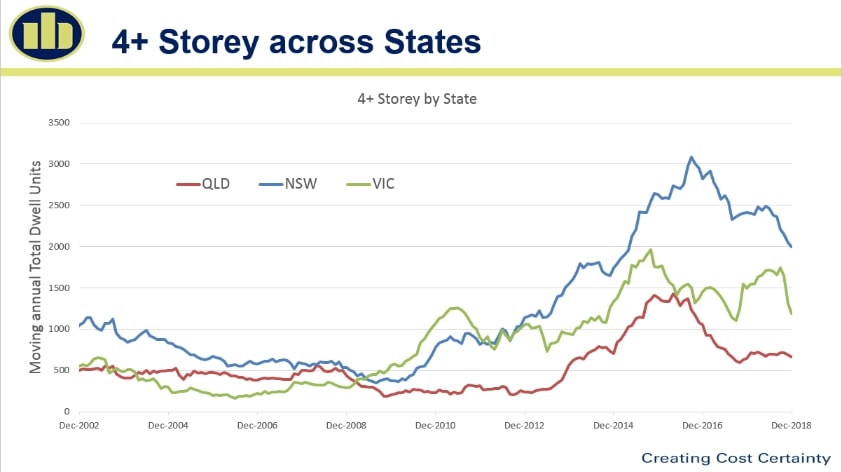

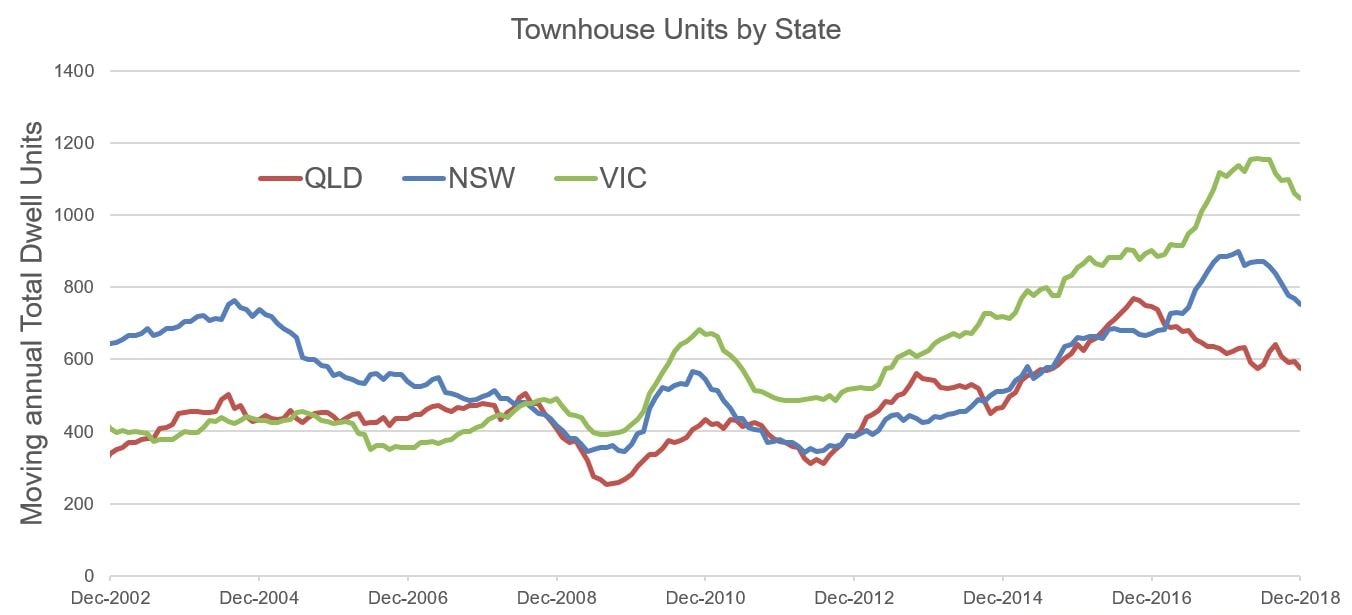

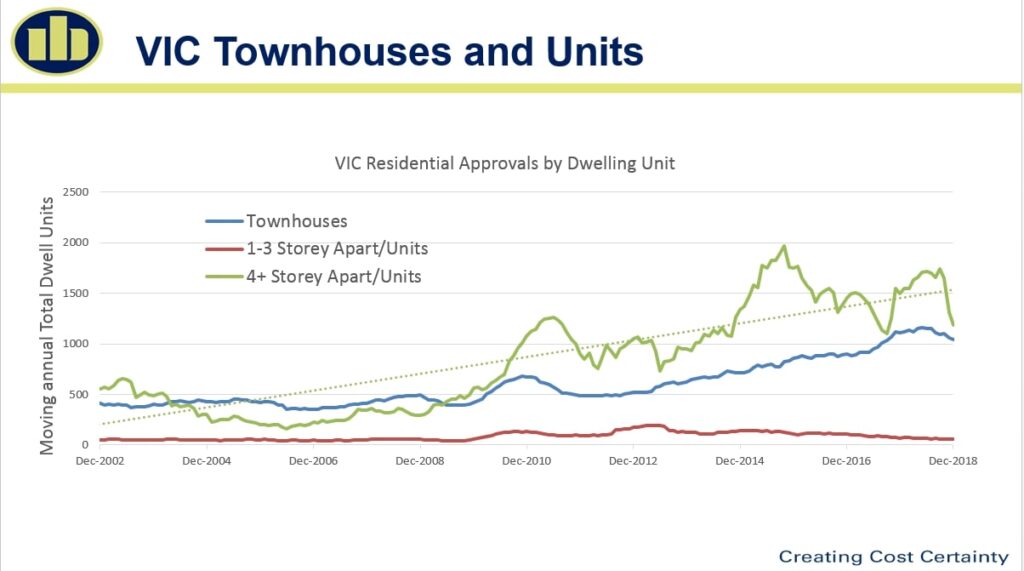

When we look at approvals of dwelling units on a moving annual basis, we can identify that approvals for both developments with more than 4+ Stories, and Townhouse product are continuing to trend downward. We are seeing that a number of previously approved dwellings will not commence in this cycle. While the number of cranes has not yet reduced, both of these factors are putting downward pressure on contractor confidence.

National Escalation Forecast

QLD Commentary

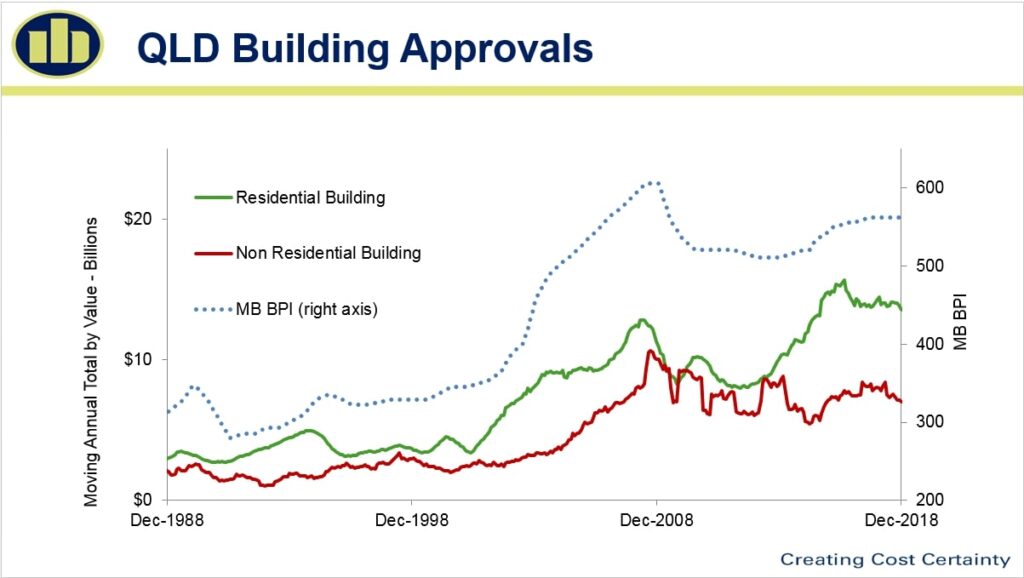

South-East QLD, and Brisbane in particular, has seen a dramatic change in the construction landscape. While there are signs that residential approval numbers have begun to bottom out, we have seen a decrease in projects under construction and that decline is going to continue to grow into the future. The market has become confident in delivering at an unprecedented volume but is now going to have to come to terms with the ‘new normal’ – which is construction levels at or about levels last seen in 2014. This is assuming that all of the projects currently being marketed (green fill on graph) reach the market at the scheduled times. This will be a challenge until we see some indications of increases in unit values, and the market understands the impact of the upcoming Federal election.

A few points to note:

1. The major banks are back and have funds available to lend for the right project

2. Project Bank Accounts (PBA’s) continue to cause uncertainty and will have a future impact on costs regardless of Govt demands for this not to happen. Contractors are already employing additional contract admin staff and there is increasing talk of a 1-2% premium on projects involving PBA’s to cover not only the administration cost but also additional funding to assist with not being able to use retention as cash flow

3. Major projects involving Union EBA’s have already locked in their increases in labour rates, however there will be increasing competition for the limited pool of subbies who are able to work on signature projects

4. The last 6 months have seen an upswing in interest from counter cyclical investors and Developers who cashed in at the height of the last cycle

5. We do not expect residential construction costs to drop off dramatically at the head contract level, although there may be some opportunity to recoup margin at the sub-contract level

NSW Commentary

NSW continues to have strong levels of construction but there have been significant falls in both residential and non-residential building approvals as the FOMO changes to FOJI (fear of joining in). This sentiment is being fanned by tighter lending conditions and decreasing valuations – which provide a self-fulling prophecy designed to keep purchasers sitting on the fence. The residential boom covering an area stretching from Newcastle to Wollongong and out as far as Penrith in the West has finally peaked and started to decline. Non-residential is also coming back off a peak, however there remains strong interest in industrial and commercial. This is impacting materials and labour that are common to both sectors.

Demand for structural trades is starting to weaken and while it is unlikely that we will see cost reductions in this space in the near term, Developers and contractors will be able to take advantage of a greater range of choice in preferred contractors. Demand for finishing trades and formwork remains strong and wages continue to rise.

Regions such as the Illawarra and Hunter continue to thrive off the back of both the growth in the Sydney market and increases in local amenity. Supply of residential apartments and subdivisions in these areas is growing in line with demand. Some units in these areas are starting to find their price ceiling and the challenge going forward will be keeping product affordable.

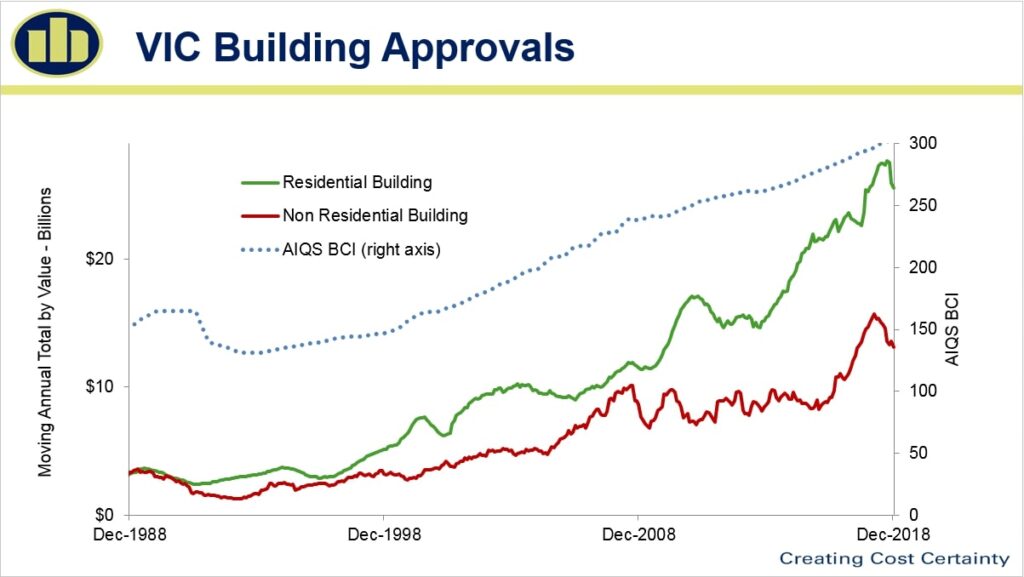

VIC Commentary

The Victorian economy remains the envy of many other States with Infrastructure, and Public spend, continuing to compete for the limelight with the residential sector. While residential is losing momentum the other sectors have at least 2 years of demand built up from population growth and the sheer volume of these works will offset any short term declines in residential.

As discussed in a previous update, the short term rally in apartment approvals experienced at the end of 2017 was largely driven by a small number of large projects and didn’t reflect the broader market. Whilst the trend is down it is still off a significant base and above the long term average trend. This has been supported by the strength of the townhouse market as owner-occupiers look for more space closer to the CBD. With the highest immigration figures for any Capital City, and both wage and job growth likely, underlying demand looks set to continue in the short term. However lack of price growth, and negative sentiment from both banks and Government is lowering Developer confidence and a number of projects will remain on the planning boards this cycle.

Developers are still able to get Contractors of choice to tender, however encouraging them to remain competitive and not walk away when they are the lowest tenderer can be problematic. Contractors are managing their book of work cautiously, instead of aggressively.

A great day to reflect and appreciate the wonderful women in our lives and the men who support us.

For International Women’s Day, the ladies in our QLD office invited some of our valued clients to join us for breakfast at The Regatta Hotel, not only to celebrate this special day but also to raise much needed funds and awareness for Women’s Health and Project Pink.

Back by popular demand… …the Mitchell Brandtman 2019 Education workshop is for Financiers who would like to gain a more thorough understanding of what a Quantity Surveyor does and how we assist Financiers and their clients on a project.

After successfully launching our Financiers’ Education Program in 2013, we are excited to now be offering these workshops again 2019. The workshops will be held in our office in Toowong and will cover off on the topics listed below:

Estimating

Check Estimates Elemental Estimating Bills of Quantities Cost per m2

Types of Building Contracts

Fixed Price / Traditional / Lump Sum Design and Construct Guaranteed Maximum Price Construction Management Cost Plus Owner Builder / Developer Builder

Understanding our Reports

Initial Reports Progress Assessments

Distressed Projects – Early Warning Signs

Insurances Bank Guarantees Dealing with Unfixed Material Project Bank Accounts

Each session will also include a site visit. We will walk you through what we look for when assessing the site on behalf of the Financier.

To register your interest, please click on your preferred date below:

Tuesday 14th May FULL Tuesday 18th June FULL Tuesday 23rd July FULL Tuesday 20th August FULL Tuesday 10th September FULL

If you have any questions in regards to the Financiers’ Education Program please email Sophie Clarke sclarke@mitbrand.com or call our Brisbane Office at 07 3327 5000 We look forward to sharing our knowledge with you and your team. The Mitchell Brandtman Team

Mitchell Brandtman team members from across our entire national network congregated at the Novotel Twin Waters Resort on the Sunshine Coast knowing that great things in business are not done by one person but by an united team

Mitchell Brandtman team members from across our entire national network congregated at the Novotel Twin Waters Resort on the Sunshine Coast knowing that great things in business are not done by one person but by an united team.

A weekend of Balloon Raft challenges, The Amazing Race ‘MB Style” and a Hawaii themed party ensured that it was a weekend our national team will never forget!

#oneteamunited#bettertogether#MB_ready

As the launch of Project Bank Accounts to the wider construction market draws near, the Queensland construction industry is being forced to address the complexities and gear up for the new environment. Mitchell Brandtman poses the questions ‘What cost impacts will this have?’ and ‘What effect will it have on the stability of the industry?

For those who may not be aware, the Queensland government states that these legal changes have been introduced to “safeguard progress payments, protect retention monies and allow for more timely payments to subcontractors”.

The intent therefore is to make sure subbies get paid and in a timely fashion, indeed one legal opinion suggests that this Act will “make Queensland legislation the most weighted in favour of claimants in Australia”.

Any time the Government intervenes in an industry, it is normally to fix a problem and oftentimes it’s a problem that the industry in question cannot fix within itself.

And so it appears within our industry today, that the amount of insolvencies and non-payments to subcontractors and the associated hardship created, has reached a level that cannot be ignored. Whether or not this legal measure will provide the solution required remains to be seen. There are mechanisms in place for review and adjustments to make sure it’s having the desired effects, but government is a broadsword not a scalpel, and it is historically slow and difficult for government to change tact mid-journey.

Our questions today are what cost impacts will this have, what effect will it have on the stability of the industry and is it likely to have the intended effect.

What cost impacts will this have?

This legislation will most likely raise costs in parts of the industry in which it’s being implemented. Not to a large degree as material, site labour and plant costs won’t be effected by this move. Financing and compliance costs are the effected inputs and head contractors will need to make sure that sufficient staff resources are available (and suitably qualified) to handle the additional compliance. The financial penalties for failure are quite steep as well as the reputational damage that could be done, so leading builders who operate in this space will want to ensure they get it right. Since this is being applied to large projects, most will require professional financing and it is certain that our financial institutions will ensure that all systems are in place to comply with legislation the same way they currently do with other due diligence issues such as insurance. The additional use of multiple accounts will further involve financial institutions in the entire project cycle and those services will need to be paid for somehow.

Any possibility that subcontractors will reduce costs as they are now more certain to receive timely payments is not likely to materialise in our opinion. All other factors that go into tender pricing remain the same, other areas of uncertainty that subbies take into consideration when pricing haven’t disappeared and, above all, subcontractors are business people. They are out to make as much money as possible from the work they do and tend to reduce tender pricing when they feel there is stiff competition or a lack of work generally. It is market forces that have the strongest effect on construction costs such as competition, innovation, an available workforce and extended economic considerations such as the general cost of living.

What effect will this have on the stability of the industry?

Currently this is aimed at larger building projects, so there are sections of the industry not effected. When introduced into the private sector in March 2019, any private sector project over $1M in value will require PBA’s, although civil, engineering and infrastructure projects are excluded. So many in the industry won’t need to concern themselves with the changes and whatever payment problems exist in those sectors will presumably continue.Most legislation has unintended consequences and it is most likely that this legislation will follow that pattern. In our opinion this will have a ‘shake-out’ effect where head contractors that do not have sufficient liquidity (or certainty of access to funding) will be caught out or be unable to effectively tender for certain contracts. Larger and more highly resourced companies will be able to use this to their advantage and effectively use the legislation to out-manoeuvre their competition. The realisation on the ground could be a period of less competition and industry consolidation with negative consequences for the companies and families on the losing end. Once everything’s bedded down, competition will continue with new and old participants slugging it out in the new reality as they always have.

While strong underlying economics continue to operate, there will continue to be strong demand for construction. Where that demand continues there will be companies willing and able to meet it and adjusting payment requirements won’t change that fundamental.

Will it have the intended effect?

There are already legal requirements in place which have varying degrees of effectiveness, some of which are ignored, flaunted or only complied with in an ad-hoc manner. Any legal requirement is only as effective to the level it is policed. Good industry players that treat their subcontractors decently and ethically have done so for many decades and enjoy the reputation and trust that comes from such behaviour. These participants would continue to do so if the laws remained the same and will do so when the law is changed. The intention is to catch the underhanded, the game players and to instruct those who may simply be uninformed as to their responsibilities. Those who are determined to behave in an unethical manner will probably continue to do so and the legislation will only be effective in such situations when there is the commensurate level of policing powers by the relevant statutory bodies.

Another aspect to consider is that of subcontractor behaviour. The intent of the legislation is to protect subcontractors, but head contractors and developers have also fallen foul of underhanded behaviour from subbies and the legislation appears to offer little in this direction. This will certainly be tested in court from multiple angles and it is certain that lawyers will do well as judges fine tune the implementation and set precedents.